On March 27, President Trump signed the Coronavirus Aid, Relief, and Economic Security Act (also known as the CARES Act), a $2 trillion stimulus package intended to help mitigate the economic devastation caused by the novel coronavirus (COVID-19).

The stimulus is good news for manufacturers, many of whom are struggling given the current economic circumstances and stand to benefit financially from the package. However, the CARES Act includes restrictions and responsibilities that manufacturers need to be aware of, especially manufacturers that produce supplies related to the healthcare industry, including ventilators, products like Personal Protective Equipment (PPE) and hand sanitizer, and medication.

We have summarized some of the key portions of the CARES Act for manufacturers.

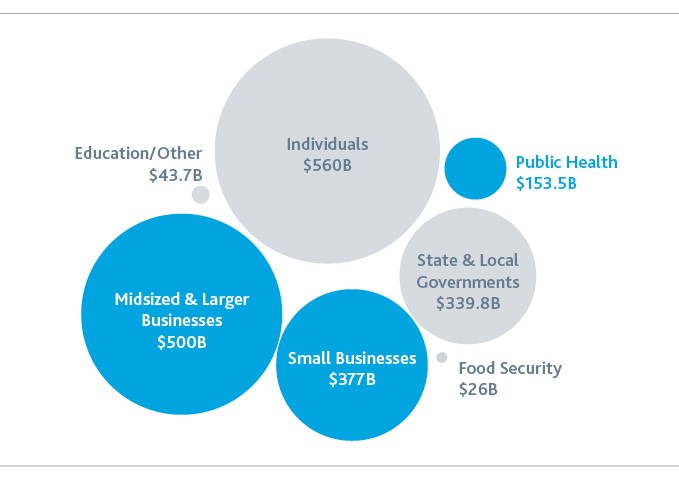

The CARES Act is comprised of multiple loan programs targeted at different groups impacted by COVID-19. The programs manufacturers may be eligible for are highlighted in the figure below.

SBA Paycheck Protection Program – $350B

Under the Small Business Administration (SBA) Paycheck Protection Program, specific funds totaling $350 billion have been set aside for small businesses, to be administered by SBA-approved lenders. Loan amounts for this provision may only be used for rent, insurance premiums, utility payments, mortgages and payroll.

In order to qualify for a loan under this program, your company must employ 500 workers or fewer (both full-time and part-time), or they must meet the industry size standard set forth by the SBA. The SBA’s size standard for auto manufacturers, for example, is 1,500 employees or fewer.

The maximum amount for these loans is 2.5 times the average total monthly payroll costs for the prior 12 months, or up to $10 million. The interest rate may not exceed 4%. Businesses can also defer payment of the principal, interest and fees for six months to one year.

One of the biggest appeals of the SBA Paycheck Protection Program is that the loans are forgivable, assuming certain conditions are met. The SBA can grant forgiveness up to the total amount borrowers spend of up to eight weeks of payroll costs and mortgage interest, rent and utility payments between February 15 and June 30, 2020, if the borrower retains its employees and does not reduce salary levels more than 25%. Loan forgiveness is prorated for organizations that do not maintain payroll. The CARES Act provides an exception to the reduction if the eligible entity re-hires employees and/or eliminates the reduction in salaries by June 30, 2020. Forgiven amounts do not need to be reported as taxable income. The Treasury Department is anticipating that not more than 25% of the forgiven amount may be for non-payroll costs.

The application is available through the Treasury Department’s website. You will need to complete the PPP loan application and include your payroll information. Once complete, submit to an approved lender by June 30, 2020.

Small businesses, not-for-profits and sole proprietorships can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders starting on April 3, 2020. Independent contractors and self-employed individuals can apply starting on April 10, 2020.

SBA Economic Injury Disaster Loans

The SBA’s Economic Injury Disaster Loan (EIDL) program gets an honorable mention here since the CARES Act temporarily expands eligibility to all businesses with 500 employees or fewer. The program offers up to $2 million in economic aid to small businesses, at an interest rate of 4% or less. Loans smaller than $200,000 can now be approved without a personal guarantee. In addition, the CARES Act removes the requirement that borrowers must demonstrate they have not been able to secure credit elsewhere.

Companies can also request an emergency grant cash advance of up to $10,000, to be funded within three days of the SBA’s receipt of the loan application. The grant does not need to be repaid, even if the candidate is not ultimately approved for a loan.

Manufacturers can apply for loans under both SBA programs as long as they do not cover the same expenses.

You can apply directly for an EIDL loan via the SBA’s online portal.

Tax Provisions

The CARES Act also introduces several tax changes, including credits, payment delays and increases to interest deductions that have immediate implications for manufacturers’ total tax liability:

Employee Retention Credit for Employers Subject to Closure due to COVID-19

This tax credit against applicable employment taxes amounts to 50% of “qualified wages with respect to each employee.”

Delay of Payment of Employer Payroll Taxes

Employers may delay their 2020 payroll taxes to be paid in full within two years.

Modification for Net Operating Losses

Tax losses from 2018-2020 can be applied retroactively five years to offset income.

Modifications of Limitation on Business Interest

Businesses may increase their interest deductions for 2019 and 2020. Previously, the maximum interest deduction was 30% EBITDA. It has been raised to 50% EBITDA.

The most important labor provisions for manufacturers are those regarding paid leave and unemployment insurance. Under the CARES Act, there is a cap on the payments an employer must pay for emergency paid leave. Employers can also elect to receive an advance tax credit on paid leave. If they do not elect to receive the tax credit, they will be reimbursed on the back end.

Unemployment insurance is available to both the unemployed and the underemployed. State short-term compensation programs will make it possible for employers to preserve pro-rated unemployment benefits for employees when reducing their hours.

Provisions to Increase Supply of Products to Help Fight COVID-19

Certain supplies, specifically hand sanitizer, PPE and cleaning products, are useful in combating the spread of COVID-19. The U.S. is currently suffering from a shortage of many such supplies. The CARES Act includes provisions intended to increase the availability of these products to protect public health.

Alcohol

There will be a temporary exception from excise tax for any alcohol that is used to produce hand sanitizer.

PPE and Hand Sanitizer Many of the funds being made available to various institutions, including the Smithsonian Institutes and the TSA, can be used for the purchase of PPE, hand sanitizer and cleaning products. The demand for these products, while high already, will likely continue to grow as government assistance becomes available for their purchase.

Takeaways

Manufacturers should now assess the need for financial relief that is being provided through this $2 trillion CARES Act. There are several very favorable loan options and tax savings strategies that manufacturers of all sizes can benefit from. The underlying theme with these loans and tax benefits is to maintain employee levels so be sure to understand these options before making decisions to reduce headcount.

For manufacturers who are able to keep facilities open, either by pivoting production or being classified as essential, employee health and safety must come first. Asking employees to take their temperature multiple times a day, to avoid interacting with other teams and to restrict themselves to their own workspace, and ensuring they know they will not be penalized for taking time off in light of potential exposure, are all important steps employers can take to reduce the likelihood of COVID-19 spreading through their facilities.

Manufacturers may consider pivoting their production to high-demand items like hand sanitizer or medical devices, which can help alleviate severe shortages of products necessary to fight COVID-19 and keep their operations running. Some manufacturers, such as perfume and alcohol manufacturers, may already have the supplies and equipment necessary to produce hand sanitizer. If you are considering pivoting your production, there are several questions you should be asking yourself first. Do you have the necessary expertise to produce the new product, or will you need to hire new workers with specialized knowledge? Are you aware of any new restrictions and/or regulations that you would be subject to if you produce this new product? Do you have access to the resources necessary to produce this product?

ORBA Welcomes New Hires to the Firm CHICAGO — ORBA, one of Chicago’s largest public accounting firms, is pleased to welcome five professionals to the firm’s Audit, Marketing, Tax and Transaction Advisory Groups.

ORBA will gladly provide you with hard copies of the useful guides listed below. Select which guides you would like to receive and submit the form below.

This booklet provides detailed explanations to help individual taxpayers, investors, business owners and professionals with tax planning throughout the year.

This website is best viewed using an updated browser, such as Google Chrome, Microsoft Edge, Firefox or Safari. Internet Explorer has been retired as of June 15, 2022, and therefore, may not allow this website’s pages to display or function correctly.

Audit

Audit

Cloud CFO Services

Cloud CFO Services

Employee Benefit Plans

Employee Benefit Plans

Health Care

Health Care

Law Firms & Lawyers

Law Firms & Lawyers

Manufacturing and Distribution

Manufacturing and Distribution

Not-For-Profit

Not-For-Profit

Real Estate

Real Estate

Restaurant

Restaurant

Wealth Management

Wealth Management