For many people, qualified retirement plans make up a large part of their overall savings. There are many complex rules surrounding qualified plans and Individual Retirement Accounts (IRAs), but there have not been significant modifications for quite some time. That may all change this year as the House of Representatives has passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, with an overwhelming show of bipartisan support. The SECURE Act passed the House by a vote of 417–3 and has bipartisan support in the Senate as well. It is expected to become law later this year.

How could the SECURE Act impact you, and what strategies should you consider if it becomes law as expected? There are a few positive aspects of the Act, including the following:

Under current law, Required Minimum Distributions (RMDs) must be taken after attaining age 70-½. The SECURE Act would increase the required age to begin taking RMDs to 72;

The SECURE Act will also eliminate the prohibition on making contributions to a traditional IRA after reaching age 70-½.;

Certain part-time workers would be eligible to participate in 401(k) plans offered by their employer. To be eligible, an employee needs to have worked a minimum of 500 hours for three consecutive years and be 21 years of age at the end of the three year period; and

Penalty-free withdrawals of up to $5,000 may be taken from an IRA or 401(k) after the birth or adoption of a child.

However, a major potential negative aspect of the SECURE Act is the elimination of “stretch” IRAs. Under the current law, the non-spouse beneficiary of an IRA can spread the distribution (and corresponding income tax inclusion) of the remaining IRA balance over their own life expectancy. This could be over 50 years for a child in their early fifties and much longer for younger grandchildren.

The SECURE Act requires that a non-spousal inherited IRA must be completely distributed within ten years of the owner’s death. There are a few exceptions which allow for a longer payout, if the beneficiary is:

A surviving spouse;

Disabled;

Chronically ill;

An individual that is not more than ten years younger than the original owner; or

Children under the age of majority.

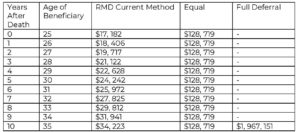

If these exceptions cannot be met, the timing and amount of income taxes are likely to be much higher, as the distributions must be paid faster and in larger increments. For example, the following chart shows the required distributions on a $1.0 million IRA for a 25-year-old beneficiary under the current rule versus the proposed ten-year rule. Note that under the current method, the beneficiary could expect another 48 years of distributions after year ten.

10-Year Rule Options 1

It also limits the decedent’s ability to utilize a trust to parse the distributions out over many years to protect a spendthrift beneficiary from themselves. The trust tax rates reach 37% at just $12,500 of income for 2019. Any IRA income not distributed to the beneficiary would be trapped in the trust at these tax rates.

Proper planning for IRAs and IRA distributions has always been valuable. The SECURE Act will make these decisions even more important, both to improve after-tax cash flow during retirement and to leave the largest legacy to your heirs.

Interested in learning more about the SECURE Act? Please join us for an ORBA Wealth Management Group’s seminar covering this and related topics on December 11, 2019. For more information or to register, visit www.orba.com.

ORBA Welcomes New Hires to the Firm CHICAGO — ORBA, one of Chicago’s largest public accounting firms, is pleased to welcome five professionals to the firm’s Audit, Marketing, Tax and Transaction Advisory Groups.

ORBA will gladly provide you with hard copies of the useful guides listed below. Select which guides you would like to receive and submit the form below.

This booklet provides detailed explanations to help individual taxpayers, investors, business owners and professionals with tax planning throughout the year.

This website is best viewed using an updated browser, such as Google Chrome, Microsoft Edge, Firefox or Safari. Internet Explorer has been retired as of June 15, 2022, and therefore, may not allow this website’s pages to display or function correctly.

Audit

Audit

Cloud CFO Services

Cloud CFO Services

Employee Benefit Plans

Employee Benefit Plans

Health Care

Health Care

Law Firms & Lawyers

Law Firms & Lawyers

Manufacturing and Distribution

Manufacturing and Distribution

Not-For-Profit

Not-For-Profit

Real Estate

Real Estate

Restaurant

Restaurant

Wealth Management

Wealth Management